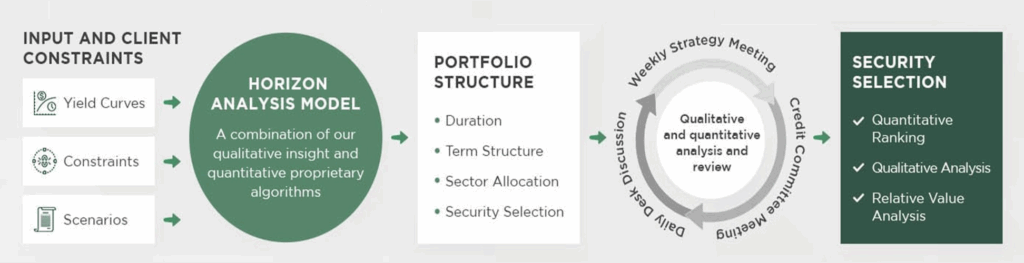

Horizon Analysis Model

We begin each engagement by understanding your liquidity needs, policy parameters, and long-term goals. Our proprietary Horizon Analysis Model simulates thousands of yield curve and spread scenarios to identify the duration, sector allocation, and maturity structure best suited to your objectives.

Inputs include:

- Current and forecasted interest rates

- Liquidity requirements and cash flow projections

- Investment policy constraints and state statutes

- Economic and credit outlooks

Portfolio Construction & Security Selection

We build high-quality fixed income portfolios aligned with your investment policy and grounded in rigorous analysis. Our security selection process incorporates:

- Credit research and issuer due diligence

- Relative value analysis across sectors and durations

- Risk budgeting and duration management

Active Oversight and Risk Management

Chandler continuously monitors your portfolio to ensure it remains aligned with your goals and policy guidelines. Our proprietary compliance systems proactively flag deviations, so you don’t have to worry about staying within the bounds of your investment policy.

We adjust strategies as market conditions evolve - rebalancing, testing scenarios, and reviewing performance - all without compromising your policy or fiduciary standards.